Nigeria’s $200 Billion Informal Economy from Street Business Fiscal Circulatory Transactions, and Reform’s Drive

Before sunrise, traders arrange vegetables in open markets, artisans unlock roadside workshops, transport operators begin daily routes and food vendors prepare for the morning rush. Across Nigeria, millions of these seemingly ordinary transactions, collectively sustain one of Africa’s largest informal economies. An economic ecosystem estimated to generate more than $200 billion annually, contributing between 55% and 65% percent to the national GDP; and provides daily incomes for nearly 90% of the country’s workforce. Welcome to the MSME “street businesses” in Nigeria.

But behind the enormous figures, lies a striking paradox. While billions of naira circulate through markets everyday, many individual traders, artisans and service providers, operate on razor-thin margins. With regards to a large share of micro-businesses, daily revenue remains below ₦20,000, leaving little or no room for savings, expansion or elasticity against inflation and economic shocks (even though an average petty-trader still manages to save something through thrift collectors).

As Nigeria’s ambitious tax reforms sails through the socioeconomic waves, expanding digital financial services and seeking to widen its revenue base, the informal economy has become more than a statistical curiosity. It now sits at the centre of debates over economic inclusion, fiscal sustainability, financial innovation and social protection. And this is an economy that official statistics only capture partly.

Note please that Nigeria’s informal sector stretches far than the traditional or ordinary open-air markets, or flea markets. It encompasses street retailers, mechanics, transport operators, tailors, food processors, domestic manufacturers, waste recyclers, mobile vendors, creative entrepreneurs, petty-traders, agricultural produce traders and millions of self-employed workers, who collectively keep local commerce moving, across Nigeria.

This wave of economic transactional-trajectory and activities, is more and more described as Nigeria’s circulatory economy. A high-frequency ecosystem, where thousands of small-value transactions create enormous cumulative economic value. Unlike large corporations that depend on formal accounting systems, the informal economy operates through continuous circulation of money. Earnings from one transaction, often finance inventory purchases in another the same day, support household expenses by evening periods, or fund cooperative savings before nightfall.

This informal economy that host rapid financial velocity and multi-status buying power, has become one of Nigeria’s strongest economic stabilizers, especially during periods of recession, inflation and unemployment.

Lagos remains the country’s largest commercial hub, accounting for approximately 16% of all informal businesses nationwide, according to industry estimates. The state’s dense population, transport networks and concentration of wholesale markets, have made it the nerve centre of Nigeria’s grassroots commercial activity. Lagos State host millions of mini-jobs, MSMEs and millions of families.

In Lagos, behind every roadside kiosk or market stall, is a homefront whose welfare depends on daily sales/incomes. Unlike formal employment, where salaries arrive monthly, most informal workers earn income from one transaction at a time. A slow business day can immediately affect school fees, rent, food purchases, healthcare spending, social lifestyle, generic bills, etc. Probably, this why public unrest or protest in Nigeria, can’t be sustained like it is seen in most other countries within/outside Africa. Millions of Nigerians believe the informal economy functions as the country’s largest social safety net.

More and more young graduates that unable to secure formal employment, are spreadingly establishing small trading businesses here and there. Within the demographic window, women dominate significant portions of food processing, retail and market commerce. Artisans provide vocational opportunities for apprentices, while transport operators connect rural producers with urban consumers, and so on. In many communities, informal businesses also finance local development through cooperative associations, rotating savings groups, market unions and community-led infrastructure projects. These grassroots institutions frequently provide credit, emergency assistance and business financing, where formal financial institutions stay absent in this interface.

However, do not think that high volume of aggregated fiscal statistics from this economic channel, means high profit or wealth, they do not always display such reality. The enormous size of Nigeria’s informal economy, can create the impression of widespread individual prosperity, but that’s not true. Some researchers would caution that transaction volume in this stead, should not be confused with profitability.

Nonetheless, many businesses record significant monthly turnover, while earning relatively modest profits after accounting for transportation costs, rent, rising fuel prices, inflation, fluctuating exchange rates, etc. Some market traders may process more than ₦1 million in monthly sales, yet retain only a small fraction as actual earnings, after replenishing inventory. So, in a hypothetical scenario, an average trader will tell you the “buyer” that he/she is sell a particular product that you are pricing, with a small margin, just to stay in business.

In respect to operators handling daily revenues below ₦20,000, even minor disruptions, such as fuel price increases, insecurity, rainy season/flooding, or supply shortages, can close-down their business entirely, or significantly reduce household income. This reality helps to explain why many informal entrepreneurs continue to operate their business regardless of the small margin, and despite seemingly impressive business volumes in aggregation.

With the evolution of financial technology-(fintech) development, cash transactions still dominates, while digital payments are reshaping commerce. Besides, in Nigeria, fintech adoption varies across user cases. While 39.5% of informal businesses use digital banks for savings, cash transactions still remains dominant. Only one in four informal businesses, which represents 25%, reports that digital payments account for 10% of their total revenue. Cash remains the preferred payment method for many informal businesses because of its simplicity, immediacy and universal acceptance.

Though, Nigeria’s expanding fintech sector is rapidly changing how grassroots commerce operates. Agency banking networks, POS terminals, mobile transfers and digital wallets, have become progressively more common across markets, transport parks, neighbourhood businesses, etc. Financial technology-(fintech) companies now process substantial volumes of retail transactions, enabling merchants to receive payments electronically, while building transaction histories that can support future access to credit.

Digital payment adoption has accelerated financial inclusion, particularly among previously unbanked, the underbanked and underserved prospects/ MSME entrepreneurs. As for most traders, digital records have become informal business statements, replacing handwritten notebooks and enabling easier access to working capital. Consequently, every expansion of digital payment infrastructure, improves transparency, while simultaneously creating opportunities for lending, insurance and business growth. This is also an inroad to managing a large economy with that ushers limited tax collection and fiscal challenge.

In reference to limited tax collection from the informal economy, and despite its enormous contribution to economic activity, much of Nigeria’s informal economy remains outside conventional taxation. Government tax revenue remains relatively low compared with the overall size of the economy, which I believe prompted the Nigerian government to seek new approaches that broaden the tax base, without discouraging entrepreneurship. Some analysts estimate that Nigeria loses billions of dollars annually in potential revenue, because large segments of informal commercial activity remain undocumented. On the reverse, many traders claim they pay multiple unofficial daily charges through market levies, transport fees, association dues and local collection agents.

To small and medium scale business owners, these acclaimed informal payments often feel like taxation without receipts, or corresponding public services. This dual reality presents policymakers with a difficult balancing act; improving revenue collection, while avoiding excessive burdens on low-income entrepreneurs.

The government’s new tax framework seeks balance within these processes. The recent fiscal reforms, attempt to formalize portions of the informal economy, while protecting the smallest businesses. Under the current framework, MSME businesses with annual turnover of ₦12 million or below, are exempted from the new presumptive turnover tax. Businesses above that threshold, may be subject to a 1 percent presumptive tax. This system is designed to simplify compliance for enterprises that do not maintain comprehensive financial records.

Government officials believe that the policy encourages gradual formalization, rather than imposing complex accounting requirements on small entrepreneurs. The wider reform agenda also includes expanded digital tax administration, unified taxpayer identification systems and electronic invoicing, for businesses transitioning into the formal economy. Also, supporters of this reform believe these measures could improve transparency, reduce tax evasion and strengthen government finances, without discouraging business growth.

However, the community of critics cautioned that implementation will determine success. Heavy-handed enforcement or multiple overlapping taxes, could undermine financial inclusion by encouraging merchants to abandon digital payments, and return to cash-only operations. An angle where, fintechs become a strategic economic partner tot eh government.

The rapid expansion of fintech has transformed payment companies from transaction processors into critical infrastructure, supporting Nigeria’s evolving tax and financial systems.

Digital financial platforms are increasingly helping merchants to maintain financial records, process electronic payments, automate bookkeeping and establish credit histories. These platforms provide opportunities to improve revenue administration, for government. While for merchants, they offer access to financial products, previously unavailable to informal businesses.

The fintech firms are also envisioned to be serving as compliance partners, automatically identifying tax-exempt micro-businesses, while simplifying obligations for larger enterprises. These systems could reduce administrative burdens and improve confidence among entrepreneurs, who fear arbitrary taxation.

On the other part of grassroots financial management approach, which has stood longer than the gen-z existence, thrift-collection has marshalled cooperative scheme that is still driving local finance continuously, till date. Long before digital banking expanded, Nigerians developed community-based financial systems known as Ajo, Esusu and cooperative savings groups. These financial scheme arrangements has remained as essential sources of capital, for informal businesses.

Members contribute regularly and access loans for inventory purchases, equipment upgrades or emergency expenses. Rather than replacing these institutions, financial technology is increasingly digitizing them. Digital cooperative wallets, transparent contribution records and mobile-based savings platforms, now combine traditional trust networks with modern financial infrastructure. This hybrid approach, may become one of Nigeria’s most important tools for expanding financial inclusion, while preserving grassroots-community-based economic practices. This cooperative scheme has been standing as an alternative window, where credit remains the missing link.

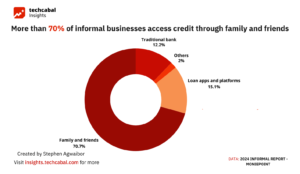

Informal businesses have persistently faced limited access to affordable financing, despite their economic importance. Traditional banks often require collateral, formal financial statements and documentation unavailable to many micro-enterprises. Consequently, entrepreneurs rely heavily on personal savings, family support or cooperative loans. So, this is the reason why financial analysts submits that transaction data generated through digital payments, could fundamentally change this landscape.

By analyzing consistent cash flows rather than traditional collateral, lenders may gradually provide short-term working capital, tailored to the realities of informal businesses. Inventory financing, supplier credit and micro-loans, could enable entrepreneurs to expand operations, hire additional workers and improve productivity.

A delicate policy balance. The future of Nigeria’s informal economy will depend largely on a right balance between regulation and inclusion. Excessive taxation, will risks discouraging macro/small/medium scale entrepreneurship, and drive informal commerce further underground. Likewise, insufficient formalization will limit government revenue-generation needed for infrastructure, education, healthcare and social services, from this informal sector. So, one would suggest that successful reforms should prioritize trust alongside compliance. This means simplifying tax procedures, reducing multiple levies, strengthening local infrastructure, improving market facilities and ensuring that increased revenue translates into visible public benefits.

When entrepreneurs perceive value from formal participation through improved roads, electricity, security and access to finance, they are more likely to embrace registration and digitalisation systems, voluntarily.

Nigeria’s informal economy is more than a $200 billion marketplace, or a percentage of GDP. It represents millions of individual ambitions, family enterprises and community networks that sustain livelihoods across urban and rural communities. Every roadside repair, market purchase, cooperative contribution and mobile transfer, reveals a larger story of robust enterprise at a macro/micro level.

As digital finance expands and fiscal reforms reshape the commercial landscape, the central challenge for government, financial institutions and development partners, will be to ensure that formalization strengthens the economic engine that supports millions of Nigerians.

If this informal economy is managed carefully and upgraded in all ramifications, integrating it into the larger financial and regulatory systems could unlock higher productivity, improve public revenue, expand access to credit and create more inclusive economic growth. However, if handled poorly, the same reforms would risk placing additional pressure on the very entrepreneurs, $$&&pkh1 whose daily transactions continue to keep Nigeria’s economy moving.

Picture Credit: techcabal | Channels TV | Webhaptic Intelligence | Tosin Adeoti Medium