African Nations Hit Hardest by Fuel Price Surges, as Citizens Bear the Brunt

Across Africa, the cost of fuel has become more than an economic statistic, it is now a daily measure of hardship for households, transport workers and small businesses. As of April 2026, a growing number of countries are showing acute sensitivity to fuel price swings, exposing profound structural weaknesses in energy systems and governance.

From Malawi to Zimbabwe, the Central African Republic to Sierra Leone and the crisscross, the pattern is consistent, heavy reliance on imported refined petroleum, pulverize currencies and limited domestic refining capacity. In these economies, even minor disruptions in global oil supply quickly translate into steep pump-price increases, pushing inflation higher and eroding purchasing power at the grassroots level.

In landlocked countries such as Mali and Burkina-Faso, geography compounds the crisis. Fuel must travel long distances over poor transport networks, inflating costs before it reaches consumers. To traders and farmers’ sensitivity, this means higher prices for moving goods, costs that are ultimately passed on to already strained communities. Island nations like Seychelles face a different, yet equally challenging reality. With no domestic production and total dependence on imports, they remain highly exposed to global supply-shocks. Each spike in international oil prices, reverberates quickly through same circumstances – electricity tariffs, transport fares, households’ bills and food prices.

Even countries with relatively stronger economies are not insulated. In Kenya and Ghana, recent subsidy reductions introduced to ease fiscal pressure, have shifted the burden directly onto consumers/the masses. In South Africa, a weakening currency has amplified the cost of imports, particularly hitting the transport sector very hard and raising concerns about wider economic competitiveness.

Perhaps most striking is the case of Nigeria. Despite being one of Africa’s largest crude oil producers, its long-standing dependence on imported refined products, has left it vulnerable to the same global shocks affecting smaller economies, which is outrightly not supposed to be the case; because, one of the largest single-train refineries processing over 650,000 barrels per day, is located in Lekki, an aspect of the coastal lane of Lagos State, and it is fully running. But, intertwined in political dynamics, leaves the grassroots to bear the daily cost of implication. In clear consideration, the Dangote Refinery and other recent investments in domestic refining, should be showing some potential turning point in easing the fuel prices at filling stations. But, the transition has not fully shielded consumers from fuel-price volatility.

The most fundamental part of this continent-wide sensitivity, is a convergence of global and domestic pressures. The heightened tensions in the Strait of Hormuz, is a critical artery for global oil shipments, which has tightened supplies and driven up prices. At the same time, weakened local currencies against the US dollar, have made imports more expensive, while subsidy rollbacks have exposed long-hidden structural costs.

Surpassing these prevailing instances, the macroeconomic indicators host a story of more human-implications. To the ordinary urban commuters, rising fuel prices mean higher fares or longer treks. To the rural farmers, it means reduced access to markets. It often translates into shrinking margins or outright closure for small businesses/SMEs. In many communities, poor electricity distribution/underperformance becomes an everyday reality.

The pressure mounts-on politically on leadership. Governments are caught between economic sustainability and social stability, and forced to balance international financial obligations with the immediate needs of their populations. The gradual removal of subsidies, which is economically rational, has sparked public discontent in several countries, highlighting the delicate social-contract between the government and citizens.

Fuel prices across East Africa have remained elevated in April 2026, with notable variations driven by subsidy policies, regulatory controls and currency dynamics. A regional comparison, standardised in Kenyan shillings per litre shows that consumers in Kenya and Rwanda continue to face the highest costs, while Tanzania and Ethiopia offer relatively lower petrol prices under different policy frameworks.

In Nairobi/Kenya, pump prices for the April-15th to May-14th pricing cycle stand among the region’s highest. Petrol is retailing at KSh 206.97 per litre, closely followed by diesel at KSh 206.84, while kerosene is priced lower at KSh 152.78. These levels keep Kenya at the top of East Africa’s fuel cost rankings, reflecting reduced subsidies and ongoing pricing adjustments. Neighbouring Uganda, as of April-13th, records moderately lower prices. Petrol sells at approximately KSh 200.5 per litre (UGX 5,290), with diesel slightly cheaper at around KSh 199. While below Kenya’s rates, Ugandan prices remain comparatively high within the region.

In Tanzania, prices capped by the Energy and Water Utilities Regulatory Authority (EWURA) as of April-1st, present a more affordable picture. Petrol averages about KSh 193 per litre, diesel KSh 188, and kerosene KSh 185, positioning the country as one of the least expensive fuel markets in East Africa, supported by regulatory controls and subsidy measures.

Rwanda, following its April-6th update, mirrors Kenya at the upper end of the pricing spectrum. Petrol is set at roughly KSh 206 per litre (RWF 2,303), while diesel stands at about KSh 197 (RWF 2,205), highlighting the country’s high import and distribution costs. In Ethiopia, government subsidies continue to influence pump prices, though outcomes are mixed. As of April-2nd, petrol is relatively cheaper at around KSh 190 per litre (ETB 142.41), but diesel rises significantly higher to about KSh 218 (ETB 163.09), making it the most expensive diesel market among the countries surveyed.

The total East Africa data highlights a region grappling with persistent fuel cost pressures. Kenya and Rwanda remain the most expensive markets for petrol, both exceeding KSh 200 per litre. Tanzania stands out as the most affordable due to capped pricing, while Uganda maintains mid-range costs. Ethiopia presents a divergent case, where petrol remains subsidised but diesel prices outpace regional averages, reflecting uneven policy impacts across fuel types.

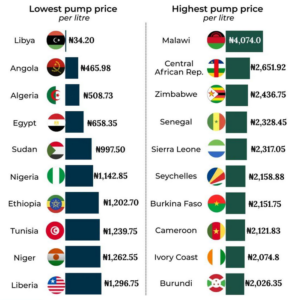

Furthermore, the fuel prices across West Africa in April 2026 reveal sharp disparities, reflecting differences in subsidy regimes, import dependence and currency pressures. Regional data shows that while some oil-producing countries maintain relatively lower pump prices, several others face significantly higher costs driven by political dynamics, logistics, taxation and global market shocks.

Across the region, petrol prices range widely from just over ₦1200 per litre in Nigeria and Niger, to more than ₦2400 per litre (exchange equivalent) in Sierra Leone, marking one of the widest intra-regional price gaps in Africa. Nigeria remains among the cheapest markets at roughly ₦1350 per litre, despite recent increases following subsidy removal and currency depreciation. Similarly, Niger, a growing oil producer, maintains relatively low prices at about ₦1214 per litre (exchange-equivalent), under a managed pricing system.

Moving up the scale, countries such as Togo ≈₦1654/litre (exchange-equivalent) and Benin ≈₦1,691/litre (exchange equivalent), sitting in the lower-middle range; while Ghana records higher prices at around GH¢13.30 per litre (roughly ₦1,800+ equivalent), reflecting recent upward adjustments in response to global oil trends.

Further increases are seen in Liberia and Guinea, where prices approach 253.90LRD Liberian Dollar per litre (₦1900 exchange-equivalent): followed by Côte d’Ivoire 780 West African CFA francs (XOF) per liter and Cape Verde 132 Cape Verdean Escudos (CVE) per litre, both exceeding ₦2000 per litre in exchange-equivalent. Landlocked economies such as Burkina Faso and Mali also record inflated prices, above ₦2060 and ₦2120 (exchange-equivalent) respectively, driven by higher transportation and supply chain costs.

At the upper end, Senegal ≈₦2,238/litre (exchange-equivalent) and Sierra Leone ≈₦2,460/litre (exchange-equivalent), rank among the most expensive fuel markets in West Africa, showing the burden of import dependence and limited refining capacity.

Overall, the oil-producing or subsidizing countries such as Nigeria and Niger, offer relatively lower prices, while import-reliant and smaller economies face significantly higher pump costs. The disparity continues to shape inflation, transport costs and household spending across West Africa, especially as global oil market volatility linked to geopolitical tensions, filters into domestic economies.

Nonetheless, the crisis is also driving-in a corridor of change. Across the continent, there is renewed urgency, around expanding domestic refining capacity, investing in alternative energy and strengthening regional fuel supply chains. These transformational change-efforts, could reduce Africa’s exposure to external shocks and lay the groundwork for more resilient energy systems, if managerially sustained with service-mentality.

However, the uneven geography of fuel price-sensitivity, emphasizes a central reality that Africa’s energy vulnerability is much about infrastructure/policy, as it is about global markets. And until these infrastructure-developmental issues are addressed, the global energy-shock burden will continue to be volatile on African countries that are least-able to absorb it.

PICTURE CREDITS: africap | Globale PetrolPrices | EANDEL